Though funny, the people interviewed in this video's lack of misinformation is shocking and terrifying. ObamaCare is what many have nicknamed the Patient Protection and Affordable Care Act, a set of health insurance and industry reforms passed by Congress and signed by President Obama in March 2010. ObamaCare has significantly increased the number of the people with health insurance coverage. It did this by overhauling the individual insurance market, where individuals buy their own policies, and expanding Medicaid, a public program that covers low-income Americans. ObamaCare however does more than expand health insurance coverage, it touches nearly every American industry.

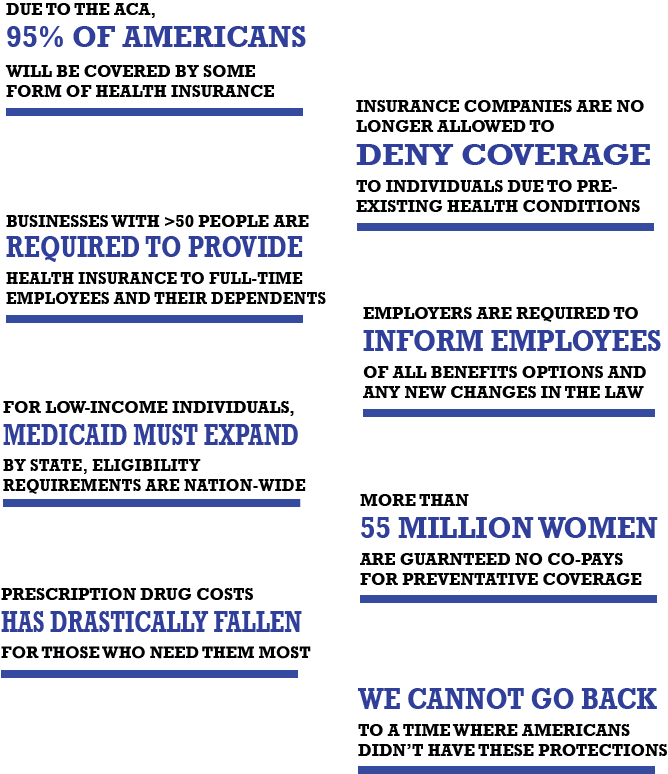

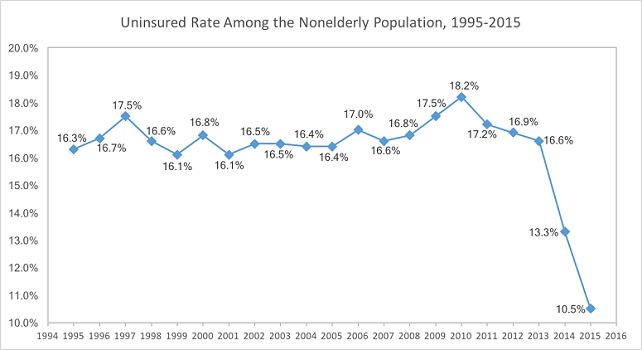

Overall, there are two main things that ObamaCare does: 1) expand access to health insurance and 2) change the way the federal government pays doctors. So far about 24 million have become insured since the expansion started in 2014 and left unchanged, the federal budget forecasters expect this number to continue to grow. When all balanced out, this means that 17 million more people have insurance that would have insurance without ObamaCare. There is another part of ObamaCare that most people do not know about. This other half of the Act launches dozens of experiments in how Medicare pays doctors, trying to link the money doctors receive to whether they improve patients’ health.

Marketplaces are supposed to make it easier to shop for coverage. Before the healthcare law was passed, it was hard to compare different policies on the individual market. There was no one place to browse different insurance plans and policies. Even on sites like EHealthInsurance, which included many options, it was hard to compare between different products. The health care law tries to make comparisons simpler by grouping all products into different metal levels: bronze, silver, gold, and platinum. Bronze is the simplest plan with coverage up to 60% of subscribers’ bills while platinum is the best with coverage of up to 90% of bills. Once somebody picks a plan on the insurance marketplace, their enrollment file gets sent electronically to the health plan, which typically collects the first month’s premium, sends out an ID card, and begins to provide coverage. In most states, the marketplace is Healthcare.gov. Only thirteen states plus the District of Columbia chose the other option and built their own marketplaces.

One can buy insurance from November 1 to January 31 and coverage can begin as soon as January 1 if you sign up before December 15. If it did, you could imagine people signing up in the most extreme conditions like en route to the hospital which would make premiums skyrocket because it would have all buying coverage at the 4exact point when they were expecting high medical bills. To prevent that, the Affordable Care Act followed many other healthcare plans, and committed to a certain time frame in which you must buy your coverage.

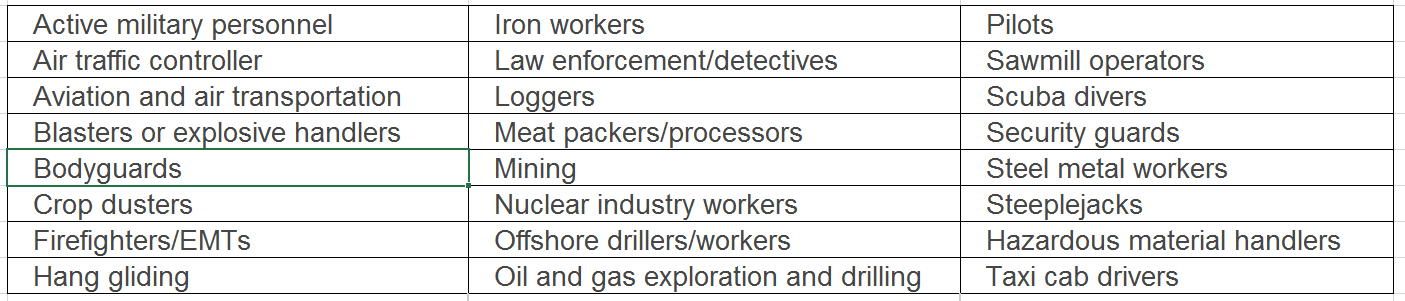

Pre-existing conditions were an insurance industry term for different medical conditions that people already have when they’re shopping for a new plan. These could range from common conditions things (like asthma) to more serious conditions (like cancer). Before ObamaCare, health plans could deny coverage or charge higher prices to people who had these pre-existing conditions. However, under ObamaCare, the concept of pre-existing conditions no longer exists. No insurance plan can reject you, charge you more, or refuse to pay for essential health benefits for any condition you had before your coverage started. Insurance companies are now barred from asking questions about applicants’ health status. They can only factor in three things — age, location, and tobacco use — in setting a shopper’s premium rate. This is why insurers believe the individual mandate is so important: they worry that if healthy people don’t have to buy health insurance, and if insurers can’t turn away sick people, then too many sick people and too few healthy people will sign up, which will create a budget deficit for the program. Once you’re enrolled, the plan also can’t deny you coverage or raise your rates based only on your health. Additionally, Medicaid and the Children's Health Insurance Program (CHIP) can't refuse to cover you or charge you more because of your pre-existing condition. It wasn't just health conditions that left people uninsured before Obamacare. Miners, oil drillers, and firefighters could also be denied because of their "health adverse" occupations. See the "Health Adverse" Occupations Chart below.

The reason people were denied coverage and treatments or charged more in the past was very simple, treating sick people is expensive. The higher the risk a customer is; the worse deal it is for the insurance company to cover them. Taking this into account insurance companies and legislators made a sort of deal. Health insurance companies would agree to cover everyone and give them all the same essential health benefits, but in return everyone who was able to afford insurance would have to buy insurance.

Everyone must obtain insurance by 2014 or pay a fee. But, think about it. If no one could be denied coverage for being sick and didn’t HAVE to buy insurance, then everyone would just wait until they were sick to buy insurance. If that happened, then insurance companies couldn’t afford to stay in business then no one would be able to afford healthcare.

Grandfathered plans don’t have to cover pre-existing conditions. If you have a grandfathered plan and want pre-existing conditions covered, you have 2 options: (1) switch to a Marketplace plan that will cover them during Open Enrollment or (2) buy a Marketplace plan outside Open Enrollment when your grandfathered plan year ends, and you’ll qualify for a Special Enrollment Period.

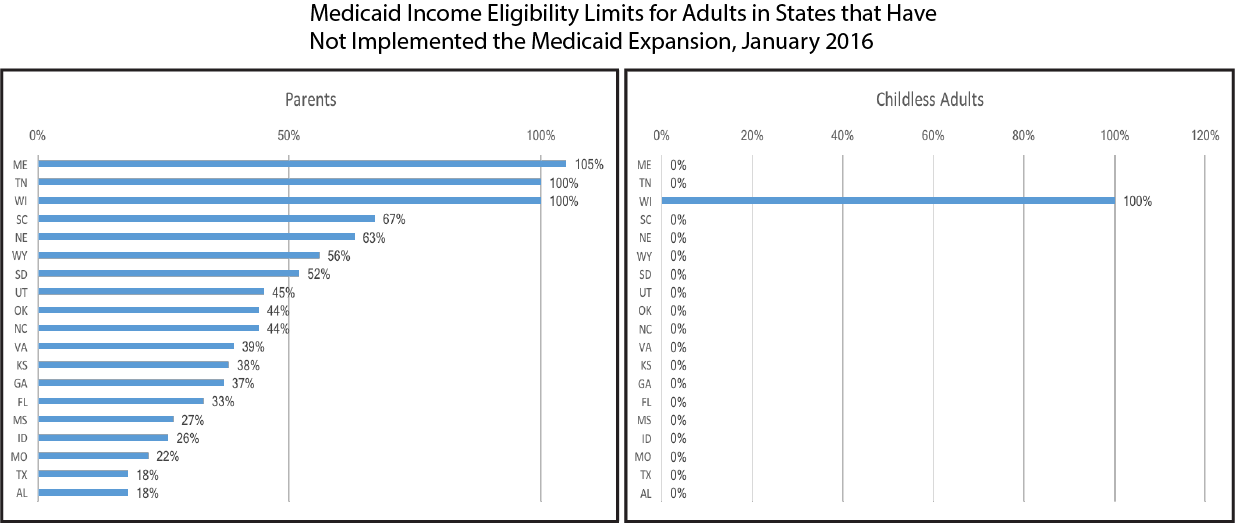

Medicaid is a joint federal and state funded program that provides health care for over 60 million low-income Americans. Before the law, Medicaid varied across the country though the Federal Poverty Line (FPL) is define US-wide—states had different eligibility requirements for Medicaid based on income, age, gender, the number of dependents, and other specific requirements. Some states had or have very narrow eligibility requirements for Medicaid, which leave many working adults uninsured. For example, parents with two children in Illinois making up to $40,700 (185% FPL) could qualify for Medicaid but an Alabama family with two children making up to $2,500 (11% of FPL) could not qualify. Poor working families are the most likely to not have insurance due to affordability. Medicaid expansion helps “cover the gap” between current Medicaid eligibility and families being able to afford private health insurance using marketplace subsidies. About half of the uninsured in America would be covered by Medicaid Expansion if all states opted in and joined the program.

The law states wanted to make more people eligible so the law contained an expansion to everyone making beneath 138% of the federal poverty line. Eligible adults are (1) non-working parents with incomes 38-138% of FPL, (2) working parents with incomes 47-138% of FPL, and (3) childless adults with incomes 0-138% of FPL. Starting in 2014 states that participated in Medicaid expansion increased eligibility levels for everyone in their state to 138% of the Federal Poverty Level (about $16,105 for an individual and $32,913 for a family of four in 2015). Even if your state didn’t expand Medicaid, you may be eligible for Marketplace subsidies if you make between 100% – 400% FPL.

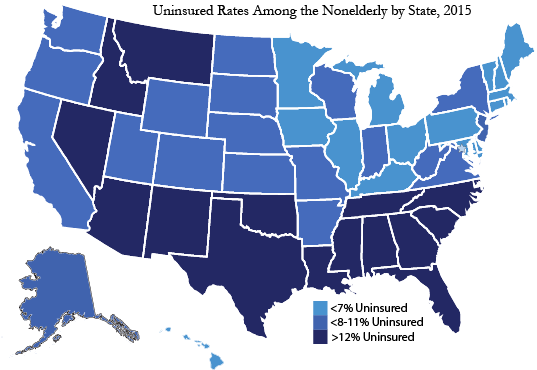

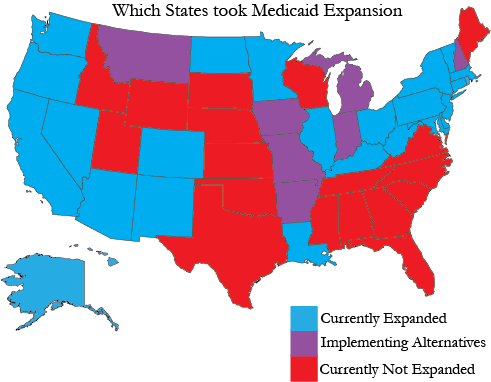

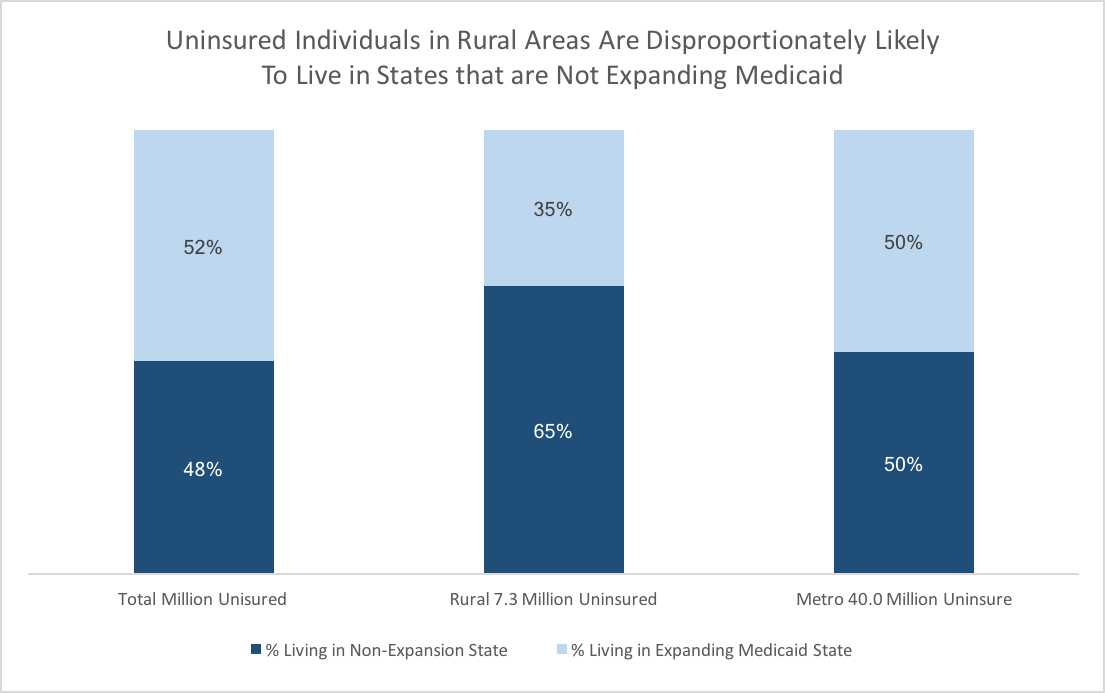

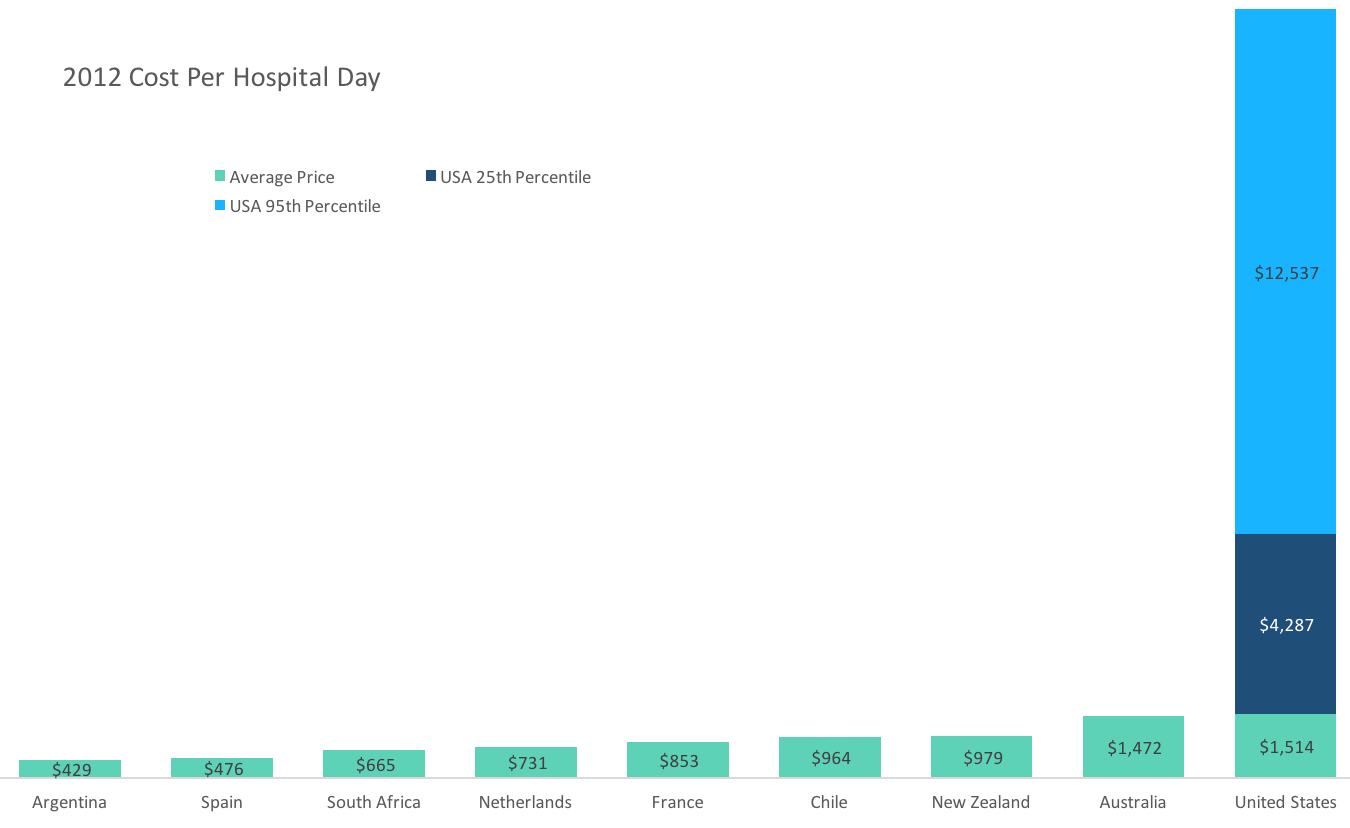

However, the June 2012 Supreme Court ruling let states reject the expansion and many states with Republican governors or legislatures have done it--so now only 28 states plus D.C. expanded. Because 24 states have not expanded Medicaid, 5.7 million people will be uninsured in 2016. Only 54% of potentially eligible adults are aware of Medicaid expansion under the Affordable Care Act. Millions of Americans will be able to get care before they are forced to use costly, last-minute emergency services. The uninsured currently cost hospitals billions in unpaid hospitals bills – some of these costs are indirectly passed onto the average taxpayer with insurance. One of the leading causes of rising premium costs is unpaid hospital bills. The Federal Government pays 100% of expansion costs for the first three years and 90% after that until 2022. Many state’s budgets have shown that expanding Medicaid raised money for the State. Cost is the most cited reason for not expanding Medicaid. While current Medicaid programs do cost state taxpayers a lot of money, that spending is balanced by unpaid hospital bills and the effect those bills have on the rising costs of premiums. In general, the states who opted out have the highest uninsured rates and would be the states which expansion would help the most. Of course, the higher number of uninsured who qualify for Medicaid, the more it costs the state to cover them.

West Virginina, under Replican Governor Tomblin, accepted the expansion providing healthcare coverage for 150,000 more residents. Governor Tomblin, not only accepted the expansion because of the coverage but also because it had NO impact on the state’s budget.

In 2015, Centers for Medicare and Medicaid Services (CMS) approved New Hampshire to convert to a Marketplace premium assistance model starting in 2016. In this model, the state obtained an authority to mandatorily enroll eligible adults in the Marketplace Qualified Health Plans (QHPs) using Medicaid as the premium assistance program.

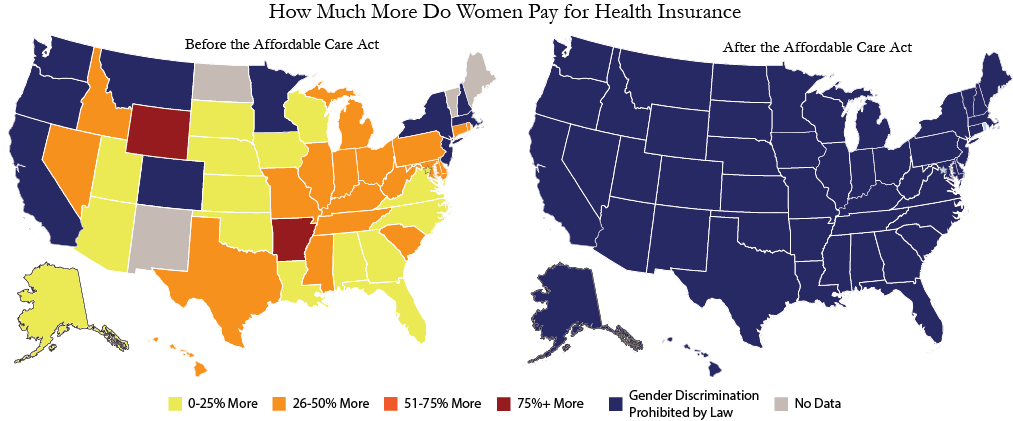

President Obama has made it clear, “ObamaCare doesn’t regulate health care, it regulates health insurance”. ObamaCare ensures that women have access to preventive services. Providing better preventive care for women will help to bring down the cost of insurance by preventing minor health issues from becoming major ones. This insurance reform helps to ensure that women stay healthy and avoid preventable medical problems. Today, women can no longer be denied coverage or charged more just because of their gender.

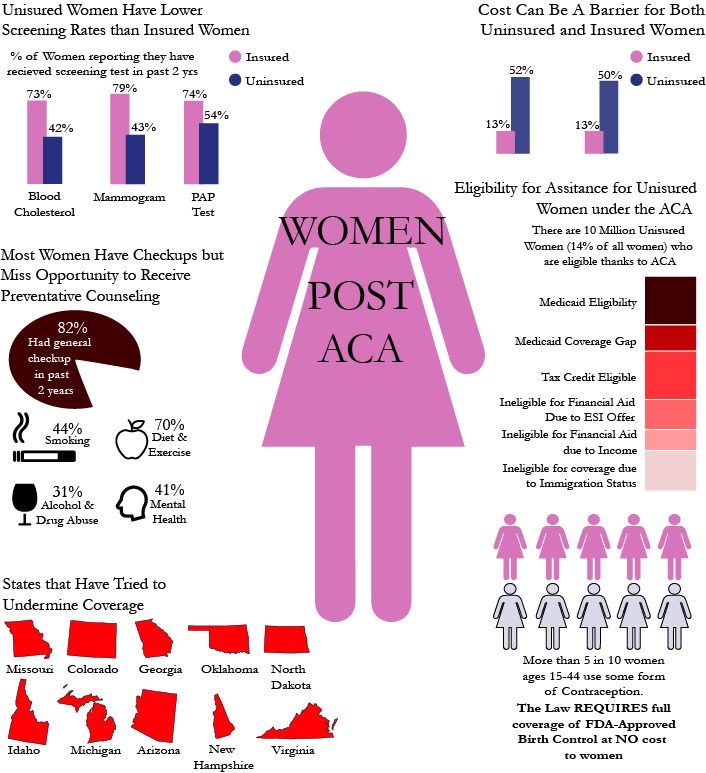

6.8 million women and girls selected affordable, quality health plans through the Health Insurance Marketplaces for 2016 coverage making it so between 2010 and 2015, the uninsured rate among women ages 18 to 64 decreased from 19.3 percent to 10.8 percent, a relative reduction of 44 percent. It has also helped the estimated 55.6 million women with private health insurance have access to recommended preventive services like mammograms or flu shots with allowing them to have no co-pay or deductible.

First, as many as 65 million women with pre-existing conditions can no longer be discriminated against or charged higher premiums for their health coverage. In the past, women could be charged more for insurance just because of their gender, and pregnancy could be defined as a pre-existing condition – resulting in denial of coverage or exclusion from certain benefits.

Secondly, an estimated 8.7 million American women with individual insurance coverage gained coverage for maternity and newborn care. About 75 percent of women entering the workforce will experience at least one pregnancy while employed. These women and their children have access to affordable, quality medical care because under the ACA, all marketplace plans must cover maternity and newborn care.

Third, the ACA accommodates nursing moms. Research shows that support for pumping at work means nursing moms are more likely to breastfeed their children, who will have better health outcomes and spend less time at the doctor. That means nursing moms will miss less work and be more productive. Under the ACA, most health insurance plans are required to provide breastfeeding support, equipment and counseling for pregnant and nursing women. Plans must also pay for breast pumps for nursing mothers.

Finally, ObamaCare covers one type of birth control per person from each of 18 FDA-approved categories at no out-of-pocket cost. Contraception can cost women up to $600 a month out-of-pocket without adequate insurance. The less money you make, the more difficult it is to pay for this. The results of health service not being available to all women equally because of cost has had a great effect on pregnancy rates, the frequency of STDs, and a number of other related issues.

If you’re pregnant when you apply, an insurance plan can’t reject you or charge you more because of your pregnancy. Once you’re enrolled, your pregnancy and childbirth are covered from the day your plan starts. If you have a 2017 health plan & give birth or adopt after you enrolled:

In a 2016 compelling journal article by CNN contributor Sally Kohn writes, "There are millions more reasons to celebrate Obamacare. Actually, at the writing of this essay, there are more than 317 million reasons — because that's the population of the United States of America and every single one of us can benefit from health care reform." She goes on to list these numbers:

As stated by Former Representative Bill Owens of New York, "The chaos that would ensue in the healthcare system by repealing ObamaCare is largely unimaginable, and I suspect not at all thought through by proponents of repeal legislation."

The fact are if Congress and the President-Elect repeal the ACA:

It is imperative that those who want to repeal the Affordable Care Act have a plan because there is no way to simply take away 20 million people's healthcare, plus take away the extended coverage provided by the ACA for many more millions of people. It is almost improbable to happen recognizing the likely public outcry and healthcare chaos that would insue. Where do those who lose coverage go for care? As you might have guessed, it is your local hospital emergency room. This will result in tens of billions of dollars in uncompensated care being provided by our hospitals. Prior to the enactment of ObamaCare, uncompensated care provided by hospitals in our communities was in the range of $75 billion to $125 billion. Would physicians continue to treat people who they knew had no coverage and no likelihood of being able to pay? if young adults ages 18 to 26 lose coverage, as well as those with pre-existing conditions, where do those who lose coverage go for care?